You are about to wire $800,000 into a U.S. real estate project you’ve never walked through, managed by a developer you met through a website, to fund a visa category that took decades to get right.

And if the project fails — or the jobs don’t materialize — you could lose both your capital and your green card at the same time.

That is the actual risk profile of an EB-5 investment. Most marketing materials skip over it. This post won’t.

Here is exactly what structural protection looks like in a real EB-5 project — and the five things you should demand proof of before committing.

The Fear No One Talks About Out Loud

Every EB-5 investor carries a version of the same nightmare.

You move your money. The project stalls. USCIS denies your I-526E because the jobs weren’t created. You’ve spent two to three years in processing limbo, paid $50,000+ in legal fees, and you’re no closer to a green card than when you started.

This is not a hypothetical. In the years before the EB-5 Reform and Integrity Act of 2022, dozens of regional center projects collapsed mid-construction. Investors lost capital. Some lost status. The program had a credibility problem.

The 2022 reform was designed to address many of those concerns, and in several important ways, it has. Regional centers now face stricter oversight. Project sponsors must file Form I-956F before associated investors submit Form I-526E petitions. Escrow protections are more clearly defined, and transparency requirements have increased across the program.

But the reform didn’t eliminate risk. It raised the floor. The ceiling — meaning how well a specific project is actually structured — still varies enormously from one offering to the next.

So the real question isn’t whether the EB-5 program is safe in theory. It’s whether the specific project you’re evaluating has real, verifiable safeguards in place.

Why Most EB-5 Investors Evaluate Projects the Wrong Way

Most investors compare surface-level details.

They look at the location, the renderings, the projected returns, and the brand name of the regional center.

Those things matter.

But they are not what determines whether your $800,000 is actually protected.

What determines protection is structure.

Specifically:

- Is the project dependent on EB-5 capital to complete construction?

- Does it have a job cushion large enough to absorb real-world shortfalls?

- Has the project sponsor filed Form I-956F and provided the required EB-5 project documentation?

- Does it qualify for the $800,000 investment threshold, or are you paying $1.05 million for something that should cost less?

These are not soft questions. They have hard, documentable answers.

And if a project can’t give you those answers in writing, that tells you something important.

How the EB-5 Program Protects Investors When a Project Is Built Right

The EB-5 Immigrant Investor Program requires a minimum $800,000 investment in a USCIS-designated Targeted Employment Area (TEA), or $1,050,000 outside one.

Your capital must be “at risk,” meaning it funds real economic activity, and the investment must directly or indirectly create at least 10 full-time jobs for U.S. workers.

That job creation requirement is the linchpin of your green card.

Miss it, and your I-526E petition — and potentially your adjustment of status process — can be jeopardized.

The EB-5 safety net isn’t one thing. It’s a stack of structural features that, when combined, can dramatically reduce the likelihood that either your capital or your immigration outcome fails.

Here is what that stack looks like when a project is built properly.

What to Look for in an EB-5 Project: 5 Safety Standards That Actually Matter

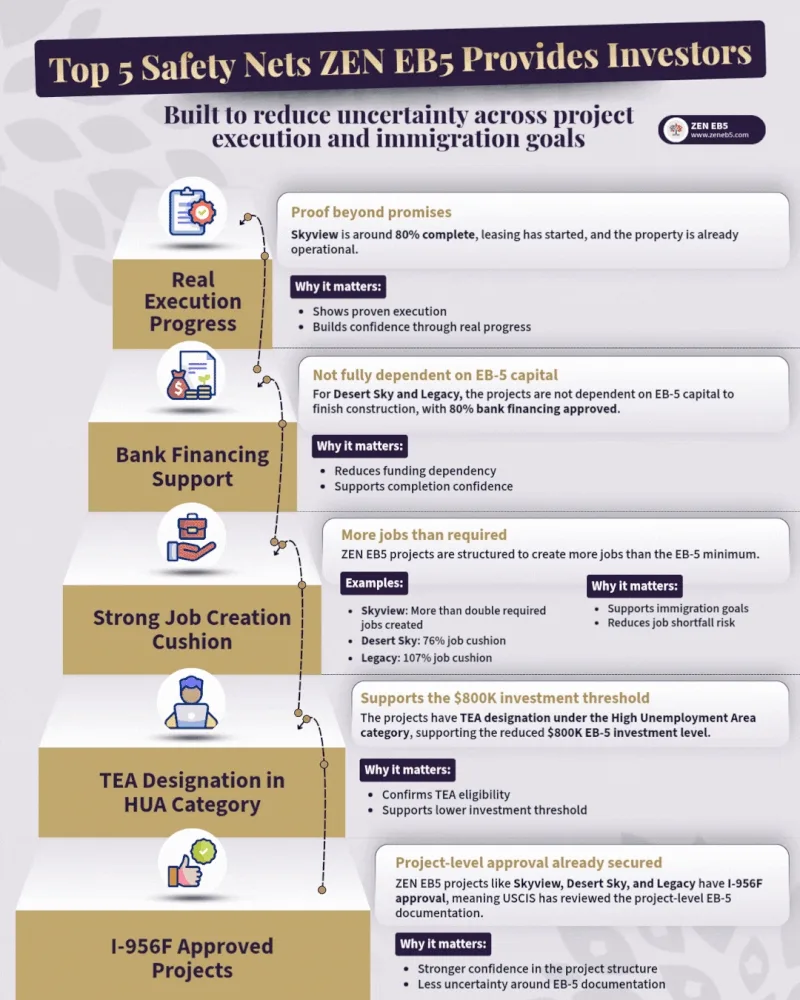

1. Real Execution Progress — Not a Pitch Deck

The single most underrated safety signal in EB-5 is construction that has already happened.

A project that is 80% complete and operationally leasing is a fundamentally different risk profile than a project that exists only in renderings and pro formas.

When a building is already up, the developer has already committed the capital, managed the contractors, and delivered results.

You are not betting on whether they can — you are observing that they already did.

Zenn@Legacy, ZEN EB5’s active project in Peoria, Arizona, sits in this category of projects where execution is not theoretical.

The 140-unit Class A multifamily development is underway in the Phoenix metro, one of the fastest-growing real estate markets in the country.

2. Bank Financing That Makes EB-5 Capital Non-Critical

Here is a structural protection most investors don’t ask about:

What happens to construction if EB-5 capital is delayed?

In a well-structured project, the answer is simple: nothing.

Construction continues because the majority of the funding is already secured through institutional financing.

When senior debt covers most project costs, EB-5 capital is supplemental rather than foundational.

That means processing delays, escrow holds, or slower investor subscriptions are less likely to jeopardize project completion.

Zenn@Legacy is structured with this kind of financing architecture, helping support completion regardless of EB-5 subscription pace.

3. A Job Creation Cushion Large Enough to Matter

The EB-5 minimum is 10 jobs per investor.

That’s the regulatory floor.

But the floor is not a safety net.

If the job count projection is exactly what is required, any variance — a slower lease-up, a contractor delay, or a revised economic methodology — can push the project below the threshold.

That creates immigration risk.

A properly structured project builds in a cushion.

Legacy carries a 107% job cushion.

That means the project is projected to create more than double the required number of jobs.

Even significant real-world variance can leave the project comfortably above the minimum requirement.

This directly supports investors’ immigration goals and reduces the risk of job shortfalls.

4. TEA/HUA Designation — The $800K Threshold Is Not Automatic

Not every project qualifies for the $800,000 investment level.

To access it, the project must be located in a Targeted Employment Area (TEA), such as a High Unemployment Area (HUA), and the designation must be properly documented.

Zenn@Legacy qualifies under the HUA category.

That matters for two reasons.

First, it allows investors to participate at the lower investment threshold.

Second, it demonstrates that the project has been structured with EB-5 requirements in mind.

5. I-956F Filing and Project Transparency

Under the EB-5 Reform and Integrity Act of 2022, project sponsors and regional centers must file Form I-956F before associated investors submit Form I-526E petitions.

The filing includes key project documentation, such as the economic methodology, job creation analysis, and offering structure.

While I-956F approval is not required before an investor files Form I-526E, many investors view an approved I-956F favorably because it indicates that USCIS has completed its review of the project’s EB-5 documentation.

An approved I-956F does not guarantee approval of any individual investor petition.

However, it can provide an additional level of confidence that the project documentation has undergone USCIS review.

Investors should still independently evaluate the project’s structure, job creation assumptions, financing plan, and compliance framework before making an investment decision.

Zenn@Legacy: Built for Investors Who Can’t Afford Uncertainty

If you are an H-1B or L-1 professional evaluating the EB-5 program as your path to permanent residency, every one of the five standards above applies directly to your decision.

Zenn@Legacy is a 140-unit Class A multifamily townhome development in Peoria, Arizona, located within the Phoenix metropolitan area.

The project is sponsored by EB-5 Coast to Coast Regional Center, qualifies under the High Unemployment Area designation at the $800,000 investment level, includes a structured three-year investment term, and carries a 107% job cushion.

The project is located near more than 100,000 jobs across major employers including Amazon, FedEx, Pepsi, and Costco, supporting the economic assumptions behind its job creation model.

It checks every box on the safety standards list above.

Not because the marketing says so — but because the project structure is designed to support those standards.

What This Means for You

The EB-5 program is not without risk.

The real question is whether the project you choose is structured to manage that risk effectively.

The difference often comes down to asking the right questions and verifying the answers with documentation.

If you are comparing projects today, start with these five standards.

Ask for information about the project’s I-956F filing status. Ask for the job creation report and cushion percentage. Ask how much of the capital stack is senior bank debt. Ask whether the TEA designation is current.

A well-structured project should be able to provide clear, documented answers.

And when it can, your decision becomes significantly easier.

If you want to understand whether the EB-5 program fits your situation, schedule a free consultation with the ZEN EB5 team at zeneb5.com/schedule/ — no obligation, just clarity.